A plain-language guide to building a 1 GW gas plant for AI compute. Read the top first. Click anything to go deeper.

Author: Bill Bubenicek, W.A. Bubenicek Development LLCReference: 1 GW gas, ERCOT, BTM ramp 2028 → full power 2031 → grid 2032Last updated: May 2026

Bottom Line

Purpose. This document bridges the gap in baseline understanding between three stakeholders building hyperscale AI infrastructure: the data center developer, the hyperscaler off-taker, and the energy infrastructure developer. Each plays a critical role; each carries different risk; each operates with capital that has a different cost, time horizon, and tolerance. The aim is shared situational awareness, so the three can coordinate optimally on capital allocation given the physical infrastructure constraints described throughout.

What this is. A reference for building a 1 GW gas plant co-located with a 1 GW hyperscale data center. ERCOT primary, PJM (Ohio/PA) comparison.

Why it's hard. Physical infrastructure (gas pipelines, transmission, large power transformers and switchgear, air permits, turbine OEMs, skilled labor, interconnection queues, water in growth regions) is the binding constraint on US AI compute through 2030. Multiple primary sources (EIA, INGAA, FERC, ERCOT, PJM, DOE, BLS, CBRE/JLL, BCG, McKinsey, S&P Global) support this view. A 4 to 7 year gas plant build cannot keep pace with a 12 to 18 month data center build, and adjacent infrastructure constraints (transformers, labor, water) compound the timeline mismatch.

How the market solves it near-term. Industry deployment patterns in 2025-2026 use behind-the-meter modular gas as a 12 to 24 month bridge to grid-tied combined cycle, in hybrid configurations supported by hyperscaler offtake commitments. This is a near-term bridge to longer-term firm-power solutions (nuclear restart and SMRs, renewables-plus-storage at firm-power scale, hybrid configurations) emerging through 2028-2032.

Firm gas transport in growth corridors is the structural input most often underestimated. Whoever holds long-tenor firm capacity controls who can build at GW scale.

Practical implication. Site quality alone is no longer sufficient to underwrite. Firm gas transport, an air permit pathway, a turbine reservation, a credible grid interconnection plan, and a hyperscale IG offtake commit are all required before financial close. The chained dependencies are the project-on-project risk; one slip cascades.

Where to read depth. Executive View (~1,000 words) → Reference Project + Master Visual → 30 Executive Summary cards → 30 Deep Dives → Takeaways.

Scope and Framing

This document is about current deployment realities and the physical infrastructure constraints affecting power and data center buildouts at AI scale. It is not a directional bet on any single fuel, technology, or sponsor. The thesis, supported by the data summarized throughout, is that physical infrastructure across multiple categories (gas pipelines and transmission, electrical equipment, water, materials, labor, permitting, interconnection, and capital) is binding on US AI compute growth through 2030 and beyond.

Gas-fired generation receives detailed treatment because it is, on current evidence, the dominant near-term bridge solution in most ISOs through 2028 (BTM modular gas, then phased simple-cycle gas turbines, then combined-cycle conversion). Gas is framed as a bridge, not a destination. The longer-term power evolution emerging through 2028-2035 includes nuclear restarts and SMR deployment, renewables-plus-storage at firm-power scale, and hybrid configurations across all three. Each of those receives proportionate coverage in the relevant sections.

The document is source-anchored where possible. Where data is genuinely uncertain (peak demand timing, technology delivery dates, regulatory direction), it is flagged as such with explicit confidence levels. Readers should treat the analysis as a current snapshot of industry conditions and a framework for stress-testing assumptions, not as investment advice.

The Three Stakeholders

The document is written primarily for three stakeholder roles that must coordinate on every hyperscale AI infrastructure project, each operating with materially different capital, risk tolerance, and time horizon. Effective coordination requires each role to understand the constraints the others operate under. The cross-stakeholder optimization is the central capital-efficiency question, covered in Deep Dive 30.

Stakeholder

Capital profile

Time horizon

Primary risk concerns

Strategic priority

Data center developer

Digital infra and real estate mandates; 25-40% dev IRR (3-4 year hold), 8-10% stabilized, long-term hold cash payback at 9-11% YoC

DC build 12-18 months; stabilization 3-4 years; lease 15 years

Site selection, construction, lease tenant credit, residual value at frontier sites

Securing IG offtake at site signature

Hyperscaler off-taker

Corporate balance sheet; very low cost of capital (~3-5% WACC); enormous scale ($500B+ combined annual capex)

Compute online date drives revenue (12-18 month deployment); willing to commit 15-20 year PPAs/leases for power

Compute timing (revenue gating), power delivery certainty, total cost of compute

Compute online date on or ahead of plan

Energy infrastructure developer

Infra fund mandates plus project finance debt; 8-12% unlevered IRR, 14-18% levered; longer holds and longer asset life

Plant build 4-7 years; stabilization 6-8 years; PPA 15-20 years; asset life 25-30 years

These three roles bring different capital with different costs of bearing different risks. The economic optimization is to assign each risk to the party with the lowest cost of bearing it. Done well, all three parties capture more value than they would in a bilateral or single-party structure. Done poorly, risk concentrates on parties that cannot efficiently bear it, capital cost rises across the stack, and projects either stall or get repriced. Deep Dive 30 covers the optimization framework in detail.

Executive View

The thesis in roughly 1,000 words. Read this if you read nothing else.

The 1 GW data center campus is a real estate project. The 1 GW power plant is an infrastructure project. Same site, same hyperscaler, overlapping but distinct investor universes (energy infra and DC infra draw from related but distinct LP bases , utility-style infra mandates with project-finance debt and longer hold for energy, digital infrastructure / real estate mandates with REIT-style economics and shorter hold for DC; the largest infra funds participate in both via separate teams and sub-strategies), completely different clocks.

A data center can be designed, permitted, and built in 12-18 months once the site is de-risked. A gas-fired power plant takes 4-7 years. The hyperscaler will not sign a 15-20 year lease without firm power. The energy developer will not commit dev capital without a signed PPA. The result is a 3-year structural gap between when the data center is ready and when the energy plant can deliver firm full power.

The 3-year gap (shaded) is the central problem the integrated DC + power model has to solve. The data center is online but underfed. The plant is partly built. The hyperscaler waits, ramps slowly, or bridges with grid backstop and modular gas.

What the market is actually trying (near-term, 2026-2028)

Three approaches are running in the field today. Each addresses one piece of the constraint; none fully closes the 3-year gap. Only one of them actually compresses physical build time. The others change ownership or financing. Beyond the near-term, the market is also deploying longer-cycle solutions (nuclear, SMRs, renewables-plus-storage at firm-power scale) covered in the Macro Limit and Three Paths to Power sections.

1. Phased ramp with modular gas. Oracle Shackelford (700 MW VoltaGrid), Meta El Paso (366 MW modular Caterpillar), xAI Memphis (27+ turbines). What it does: compresses time to first compute by deploying reciprocating engines in months rather than years. Phase 1 power lands in 12-18 months from NTP, well before H-class turbines arrive. What it doesn't do: it doesn't compress time to full 1 GW, that still takes 4-7 years. This is the dominant near-term strategy for compressing the compute deployment date (see Deep Dive 22 Assumption 4 for alternatives , nuclear restart, SMRs, grid arbitrage , and their constraints).

2. Hyperscaler vertical integration. Google's ~$4.75B acquisition of Intersect Power's digital power assets (reported Dec 2025; verify exact terms before any external use). What it does: removes the counterparty negotiation friction. One party now owns both sides. Captures all power margin internally. What it doesn't do:does not compress the physical build timeline. Owning the developer doesn't make permits faster, turbines arrive sooner, or pipelines build quicker. Google still waits 4-5 years for full power. The strategy changes who owns the value chain, not how long the chain takes.

3. Utility partnership. Meta Richland Parish with Entergy ($3.2B utility capex, $10B+ Meta DC). What it does: regulated-utility credit improves financing, capacity market revenue (in PJM) adds a second revenue stream, and risk shifts onto the utility ratebase. What it doesn't do: doesn't compress the build. Same 4-5 year physical timeline.

Phased modular gas is the dominant near-term accelerator through 2028, with the alternatives (nuclear restart, SMRs, grid headroom arbitrage, transmission expansion, renewables-plus-storage at firm-power scale) covered in Deep Dive 22 Assumption 4 and the Macro Limit section. Vertical integration and utility partnership help with coordination, financing, and margin capture, but they do not by themselves close the 3-year gap. That gap is structural and physical, driven by permits, pipelines, transmission, transformers, turbines, water, and EPC labor, none of which respond to ownership structure alone.

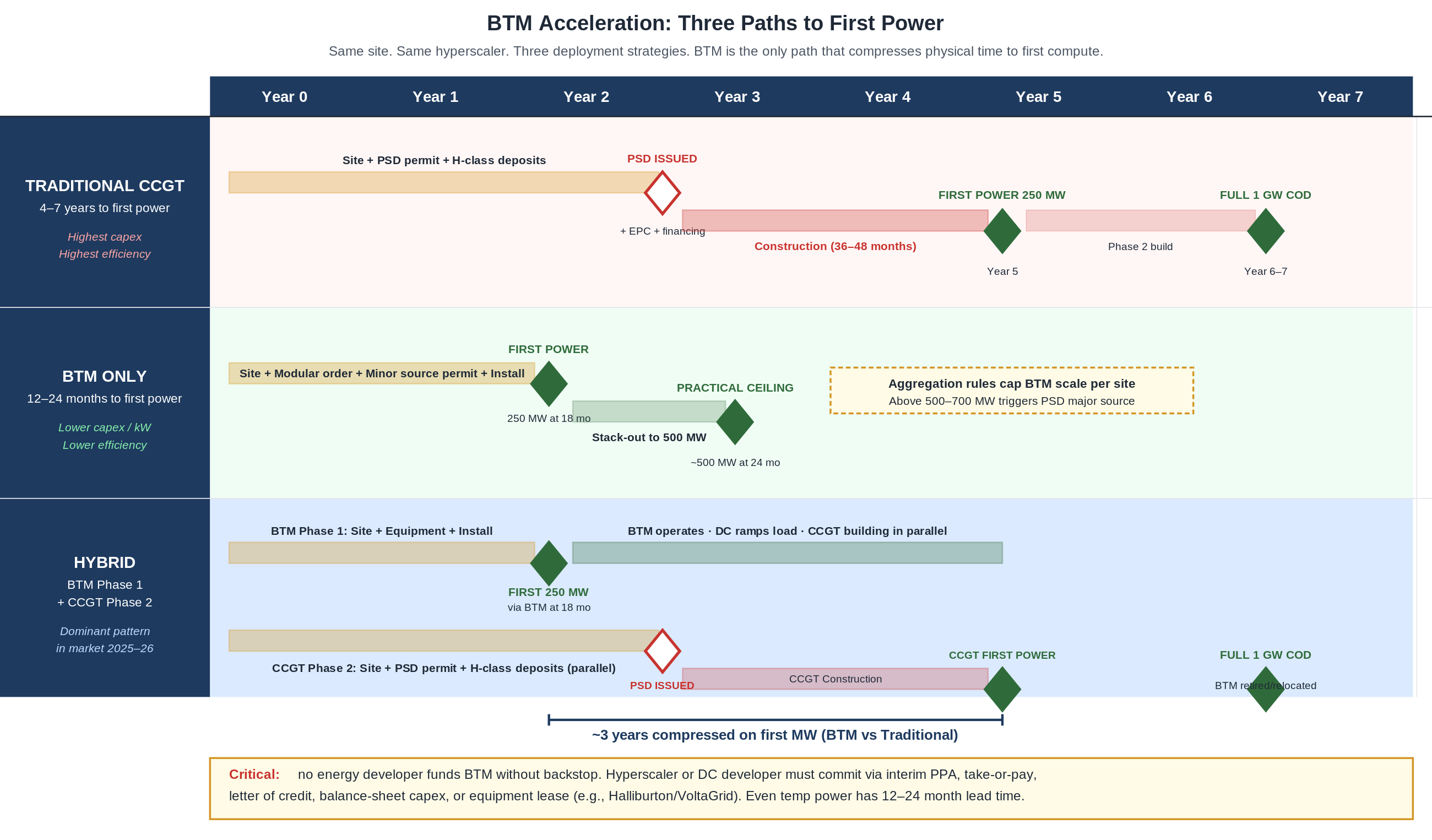

The path forward: BTM acceleration as near-term bridge

The 3-year gap is closed in practice today by behind-the-meter (BTM) modular gas, framed as a near-term bridge rather than a permanent destination. The dominant deployment pattern compresses physical time to first power, from 4-7 years for traditional CCGT to 12-24 months for modular reciprocating engines (Wärtsilä, Caterpillar, INNIO, deployed via VoltaGrid and similar integrators). Every major hyperscale project shipped in the last 18 months has used some form of BTM gas, and most pair it with a planned transition to grid-tied CCGT or alternative firm-power solutions over a 5-10 year horizon.

Same site, same hyperscaler, three deployment strategies. BTM compresses ~3 years out of the path to first compute.

What's different about BTM:

Capital outlay compressed. Typical minor-source BTM deployment: $700M-$1.2B for 500 MW in 12-24 months. Larger BTM (1 GW+) is possible under PSD major source review (adds 18-24+ months to the permit; capex scales roughly linearly to ~$1.4-2.4B). Compare to traditional CCGT: $2.5-3B for 1 GW in 4-7 years. Lower per-kW upfront for BTM, but lower efficiency over life.

Backstop is non-negotiable. No energy developer funds BTM without hyperscaler or DC committing via interim PPA, take-or-pay, letter of credit, balance-sheet capex, or equipment lease (Halliburton/VoltaGrid pattern). The backstop is the project.

Underwriting changes for both sides. Energy: 7-10 year PPA tenor vs 15-20, 40-50% sponsor equity, debt premium 200-300 bps, IRR target 12-15% vs 8-12%. DC: same dev IRR (25-40%) but compute-online date moves up 3 years.

Hybrid (BTM Phase 1 + CCGT Phase 2) is the dominant pattern. Reference project uses this. BTM compresses time to first compute. CCGT delivers full 1 GW long-term. BTM gear retires or relocates when CCGT comes online.

The headwinds are real. BTM has structural efficiency penalty (35-42% vs CCGT 50-64%, 25-40% higher fuel cost per MWh), recip-engine emissions/permitting scrutiny per MW (1.5-3× CCGT), relocation cost on hybrid timelines ($200-400/kW), and short-tenor PPA fuel-price exposure that compounds in tight basins. Section 18 covers the downsides explicitly. BTM wins on speed , it does not win on lifetime economics.

Full treatment in Deep Dive 18 (BTM Acceleration). The standalone BTM_Analysis document covers the case in greater depth.

The financial disjointedness

The DC and energy plant don't just have different timelines, they have different cash flow shapes. The DC reaches stabilization in 3-4 years (developer hold-to-flip model, exit at cap rate captures 25-40% dev IRR). Full cash payback at typical 9-11% yield on cost is closer to 9-11 years for a long-term hold. The energy plant reaches stabilization in 6-8 years. Either way the misalignment between the two timelines forces separate financing structures or term-matched deals. The capital-efficient solution is cross-stakeholder coordination: allocate each risk to the party with lowest cost of bearing it, given the three roles' different capital costs (DC developer at 25-40% dev IRR, energy developer at 8-12% unlevered, hyperscaler at near-balance-sheet cost) and different time horizons. Deep Dive 30 covers this framework.

Directional shape only, not a financial model. The DC trough is deep but short (sharp inflection at COD year 3). The energy plant trough is deeper and longer (4-6 years of negative, partial revenue mid-trough, full revenue much later). Two cash flow shapes that do not naturally share one capital stack.

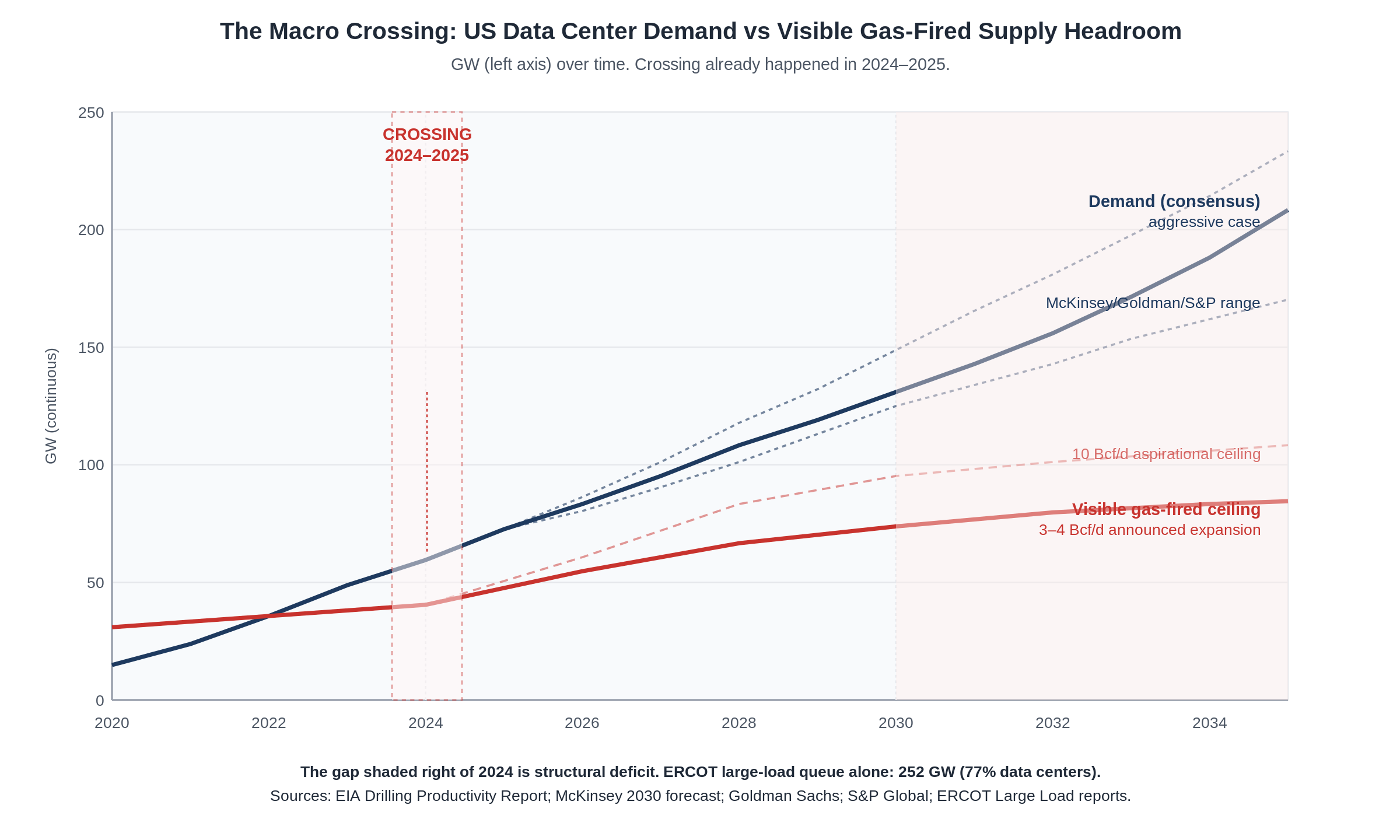

The macro limit

The United States has already crossed the point where data center power demand exceeds visible new gas-fired supply.

The numbers, validated against EIA, McKinsey, Goldman Sachs, S&P Global, and ERCOT filings. Confidence levels and the logic behind each estimate are stated explicitly so the reader can stress-test the assumptions:

US natural gas production: ~118 Bcf/d total in 2025, three top basins ~79 Bcf/d (Marcellus/Utica 36.6, Permian 27.7, Haynesville 14.9). Confidence: high (EIA reported).

Gas-fired supply headroom for new data center load through 2030: announced 3-4 / realistic 5-8 / theoretical 10+ Bcf/d (~19-25 / 32-50 / 63+ GW equivalent). The realistic 5-8 Bcf/d (~32-50 GW) is the working assumption for the rest of the doc. Three views, all stated:

Announced floor: 3-4 Bcf/d / ~19-25 GW.Confidence: high. Conservative visible/committed only , counts named, FERC-filed pipeline projects (Mountain Valley Pipeline Boost ~2 Bcf/d 2028, Greene Interconnect ~1 Bcf/d 2028, Boardwalk/Gulf South storage). 2026 is shaping up as the largest US gas pipeline buildout year since 2008 (~18 Bcf/d planned total additions across all sectors per INGAA), with East Daley and similar trackers identifying ~3-6 Bcf/d as the credible DC/power-tied range , the high end of which sits within the "realistic estimate" below. The 25 GW conversion assumes modern combined-cycle efficiency at ~7,000 BTU/kWh, ~49% LHV (1 Bcf/d ≈ 6.3 GW continuous).

Realistic estimate: 5-8 Bcf/d / ~32-50 GW.Confidence: moderate. Builds on the announced floor by adding capacity that is not yet in formal FERC filings but has line of sight: intra-basin gathering and processing additions (compression upgrades, looping that doesn't need new mainline FERC), M&A on existing systems, LNG redirect (if LNG netbacks compress, gas redirects to domestic power), and pre-FERC announced projects. This range is the working assumption for the rest of the doc.

Theoretical ceiling: 10+ Bcf/d / ~63+ GW.Confidence: low. Achievable only with active policy intervention , DOE Section 202(c) emergency orders, FERC fast-tracks, or Trump-administration emergency action. Not currently in market.

Demand:

Current US data center demand: 30-62 GW total electricity load (S&P high, Bloomberg/LBNL low) , this is total power including grid + renewables + existing gas, not pure incremental gas-fired headroom. Confidence: high on operational base, moderate on upper bound.

2030 consensus demand: 70-100 GW (McKinsey, Goldman, S&P). Aggressive end 100+ GW. Confidence: moderate. Forecasts have been revised UP every 6 months for 3 years; could surprise high (more Stargate-class commits) or low (algorithm efficiency, demand normalization).

ERCOT large-load queue: 252 GW as of early 2026, 77% data centers, 4-5 year wait , figure fluctuates with each filing. Confidence: high.

Dominion paused new large-load interconnections through January 2026. PJM closed new interconnection requests for nearly four years. Confidence: high.

The implication: even at the realistic 5-8 Bcf/d estimate (~32-50 GW headroom), demand at 70-100 GW outruns supply by 20-70 GW. The deficit is real across all credible sensitivities. Only at the theoretical 10+ Bcf/d ceiling combined with low-end demand does the gap close , and that requires both supply policy intervention AND demand normalization.

See Deep Dive 22: Assumptions, Confidence Levels, and Sensitivities for full methodology and what changes if any of these assumptions is wrong.

The crossing happened in 2024-2025, early strains binding now, deepest shortfall projected 2027-2028. Demand already exceeds announced incremental supply by 30-40 GW. The market is responding now: queue saturation, behind-the-meter pivots, hyperscaler vertical integration, $4.75B acquisitions of clean-energy developers. The deepest deficit is still ahead, forecast for 2027-2028 when AI training and inference peak against still-constrained physical infrastructure.

Chip efficiency does not save you

Nvidia's GPU progression V100 → A100 → H100 → H200 → B200 has delivered ~9× perf-per-watt over 8 years. Extrapolated to 2030 that's another 2-4×, plus 1.5-2× more from low-precision training (FP8, FP4). Realistic total: 3-8× by 2030. But demand grows ~20-25% annually (front-loaded and lumpy , large hyperscaler commits land in step changes, not smooth curves) and efficiency grows ~30-40% annually on AI workloads. At the aggregate scenario level they roughly cancel; in any specific year they may not (a Stargate-class commit can blow through a year of efficiency gains in one quarter). See Deep Dive 22 Assumption 3 for the hardware × algorithm sensitivity table. Even at 5× efficiency improvement, the gap doesn't close, because the constraint is physical infrastructure (pipelines, transmission, permits, turbine OEMs, EPC labor), not silicon.

Five takeaways

The data center and the power plant run on different clocks, 12-18 months vs 4-7 years. This is the central structural problem.

The 3-year gap is bridged by phased ramp, vertical integration, or utility partnership, every successful project picks one.

The supply ceiling has already been hit, in 2024-2025. ERCOT and PJM are the canaries.

Chip efficiency is not the lever. Physical infrastructure is.

Hyperscalers are now power developers. Google-Intersect at $4.75B is the template. Expect more.

Reference Project

One illustrative scenario, not a universal template. Real projects vary on every dimension: region, scale, off-taker credit, multi-tenant vs single-tenant, and configuration. This reference is the most replicable pattern in market 2026 (1 GW gas + 1 GW DC, ERCOT, single IG hyperscaler, BTM Phase 1 to grid Phase 2). It reflects one configuration of three-stakeholder coordination (DC developer plus IG hyperscaler off-taker plus energy developer with phased ramp). Deep Dive 22 covers sensitivity to alternate scenarios; Deep Dive 30 surveys alternative stakeholder configurations (hyperscaler vertical integration, utility partnership, OEM equipment lease) observed in market 2025-2026.

Comparisons to PJM (Ohio, Pennsylvania) appear where rules differ.

Total power

1,000 MW (1 GW) natural gas-fired

Plant configuration

Phased: fast-deploy modular generators for first power, H-class combined cycle for full 1 GW

Location

ERCOT (Texas)

Operating mode

Behind-the-meter (BTM) during ramp; grid interconnect after full power

First power

2028 (Phase 1, ~250 MW)

Full power

2031 (1,000 MW)

Grid backstop online

2032

Off-taker

Single hyperscale data center, build-to-suit

Off-taker credit

Investment grade (top-tier hyperscaler proxy)

BESS

Co-located, sized for AI ramp (100-500 MWh)

Black start

Required

Renewables overlay

Excluded from base case

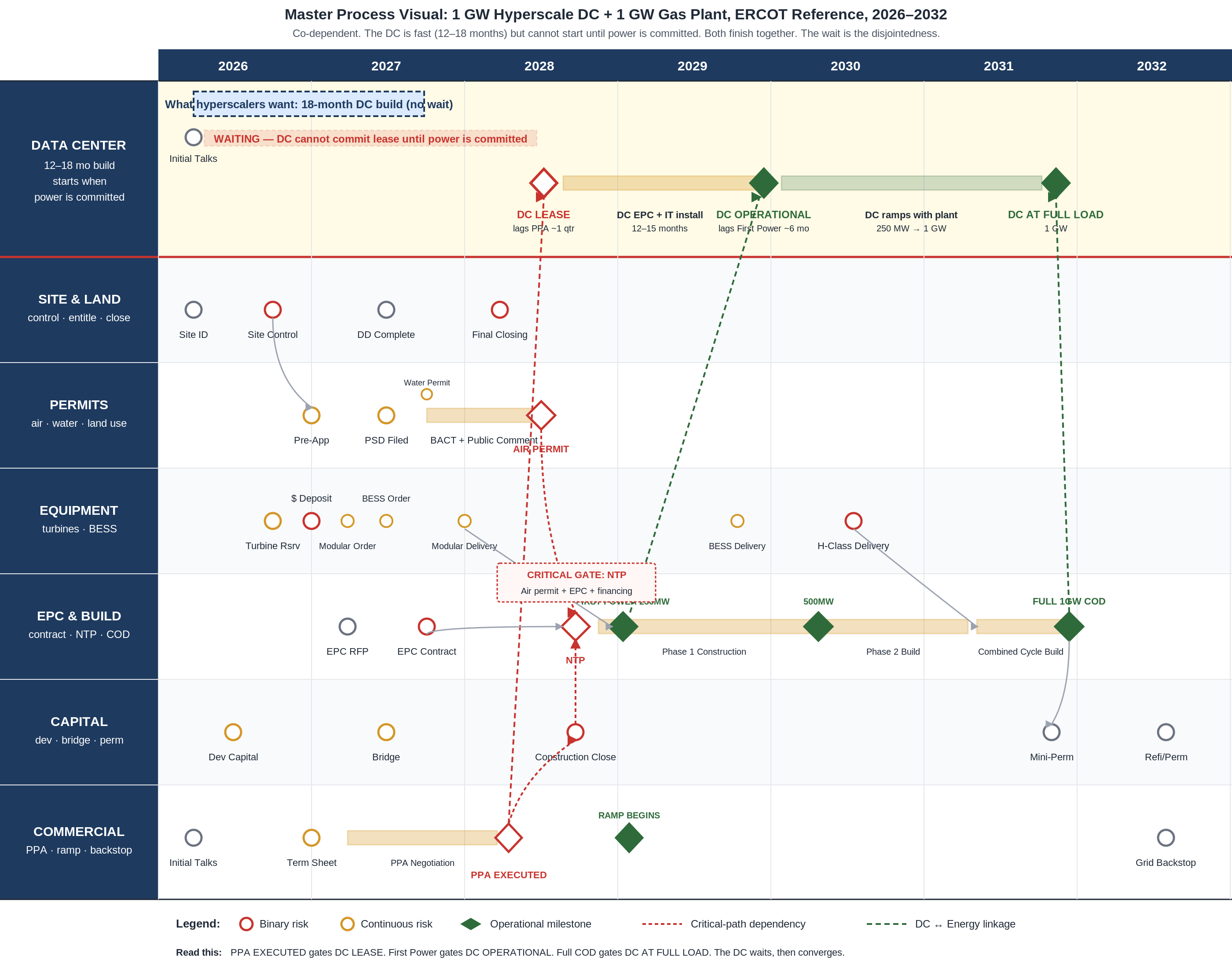

The Master Process Visual

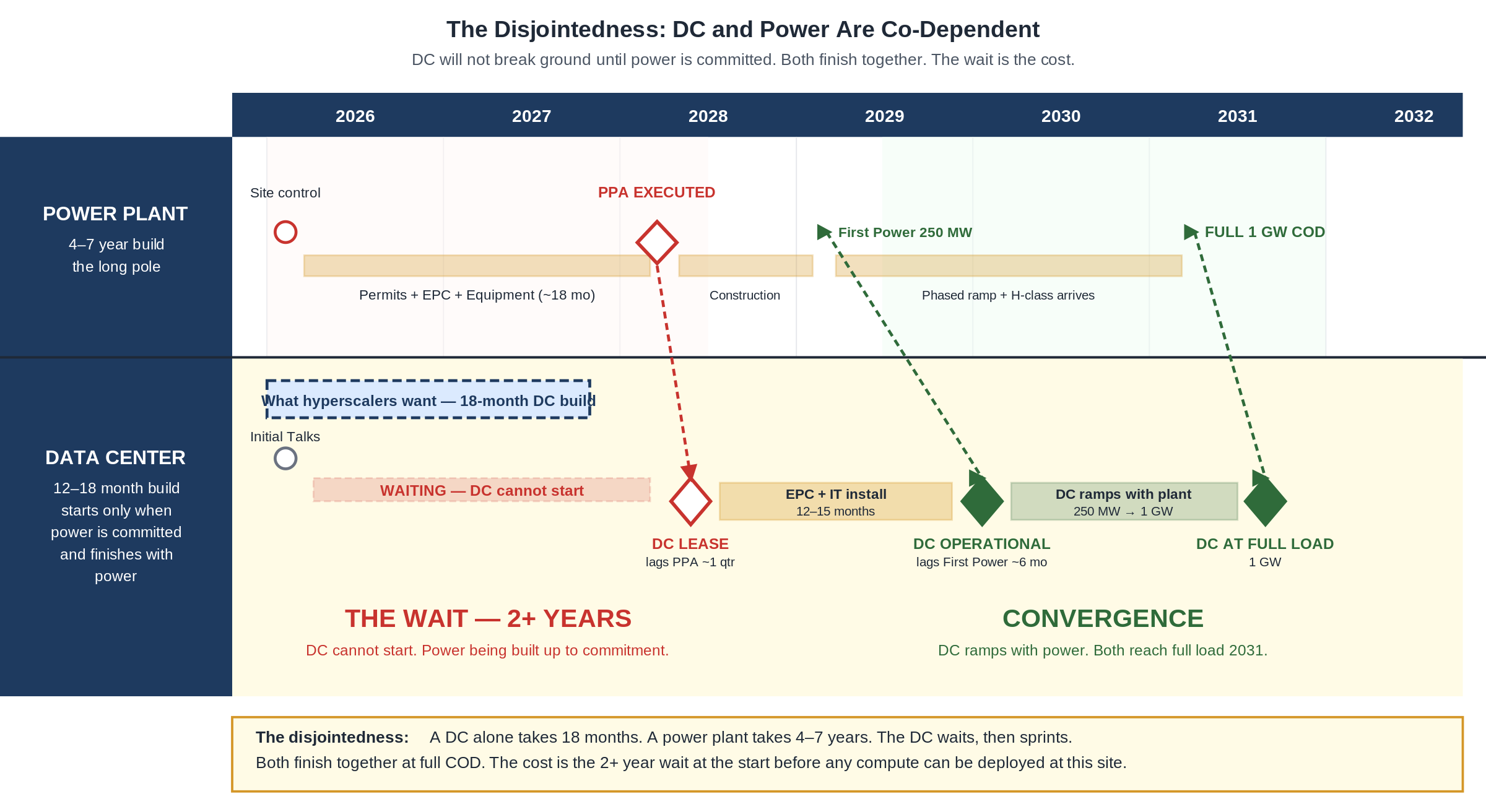

The DC and energy timelines on one page, with every chained dependency marked. Where the project-on-project risk lives.

Seven lanes side by side: a DC overlay lane on top showing the data center timeline, plus six energy plant lanes (Site & Land, Permits, Equipment, EPC & Build, Capital, Commercial). Each milestone is a node. Binary risks are red. Continuous risks are amber. Vertical dashed dependency lines show the gating between energy and DC milestones.

Top yellow lane shows the DC. Six lanes below show the energy plant. Red dashed arrows mark critical-path dependencies. Vertical dependency lines from the energy lanes up to the DC lane show co-dependency: PPA EXECUTED gates DC LEASE, First Power gates DC OPERATIONAL, Full COD gates DC AT FULL LOAD. The "Ghost" overlay at top of the DC lane shows what an 18-month DC build would have looked like if power existed Day 1.

Executive Summary

Thirty cards. One paragraph each. The full risk and design map, scannable in five minutes.

One headline per part of the project. The single most important truth. Click any card to jump to the deep dive.

Each card above expanded with sources. Read the ones that affect your role.

Each section answers the same five questions: What it is, Why it matters, Interdependencies, Risk type and magnitude, Underwriting impact.

01, Three Paths to Power

What it is

Every hyperscale data center needs firm power at gigawatt scale. There are only three ways to get it: build new generation on fresh land (greenfield), convert an existing power plant (often a retiring coal plant or under-used gas peaker), or interconnect through a creative grid arrangement such as co-location with an existing nuclear or gas plant. Most real projects mix two or all three.

Why it matters

Each path has very different economics, timelines, and risk. Greenfield gives you maximum control but takes 4-7 years and carries full permitting risk. Conversion is faster (18-30 months) and uses existing infrastructure but is constrained by what the original site allows. Co-location can deliver power in under 18 months but is exposed to evolving FERC rules. The Amazon-Talen Susquehanna deal had to restructure into a "front-of-meter" framework in spring 2026 after FERC challenged the original co-location structure.

Interdependencies

The path you choose drives air permitting (greenfield needs full PSD; conversion may reuse a permit; co-location may avoid new air permits entirely), capital stack (greenfield holds dev capital at risk longest), and off-take credit (co-location with IG-rated operators like Constellation or Talen commands better terms than an independent producer).

Risk

Mixed. Greenfield carries binary permitting and continuous supply chain risk. Conversion carries existing-asset condition risk. Co-location carries binary regulatory shift risk, the FERC December 2025 colocation order is still being implemented. Magnitude: choosing the wrong path can add 2-5 years and $500M+ to total cost.

Underwriting impact

Greenfield gas requires the deepest dev-capital discipline (5-10% of total cost held at risk for 24-36 months). Conversion projects often qualify for refurbishment financing with shorter dev periods. Co-location debt sizing depends almost entirely on the existing generator's IG credit rating.

The longer-term mix: nuclear, renewables-plus-storage, hybrids

Gas-fired generation is the dominant near-term path because of build-time advantages. The firm-power mix is anticipated to evolve through 2030-2035 with material contribution from non-gas sources:

Nuclear restart and SMRs. Existing US nuclear is ~95 GW operating; 5-8 GW of additional restart potential by 2030 (Three Mile Island via Constellation-Microsoft, Palisades, Diablo Canyon and similar), subject to NRC approvals and ISO interconnection timing. SMR deployment (Kairos, X-energy, TerraPower, NuScale, GE Vernova BWRX-300) is forecast in industry analysis at 10-30 GW US potential by 2030, contingent on lead deployments hitting milestones in 2026-2028. Confidence: moderate on nuclear restart timing; low on SMR delivery dates given historical slippage.

Renewables-plus-storage at firm-power scale. Solar and wind plus 4-8 hour battery storage do not deliver 24×7 firm power equivalent to gas or nuclear for AI training loads, but can supply meaningful capacity for inference workloads, grid backfill, and partial offset. Industry analysis (NREL, BNEF) suggests storage durations need to extend to 8-12 hours plus to compete on firm-power economics, which is a 2028-2032 horizon. Confidence: high on near-term limitations; moderate on long-duration storage trajectory.

Hybrid configurations. The dominant emerging pattern: gas as anchor firm power, with solar-plus-storage providing offset and capacity-market participation, plus nuclear or SMR as longer-term replacement of the gas baseload. Reference projects: Meta Richland Parish (Entergy gas anchor with renewable offset); Microsoft / Constellation TMI restart (nuclear replacing gas in the firm baseload role); Google / Kairos SMR (early-stage nuclear development as part of a longer-term mix). Confidence: high on the directional trend; moderate on specific deployment economics.

A site is not a piece of land. A site is the combination of six dimensions that have to all line up at the same place. The site qualification checklist below mirrors a standard internal diligence framework used in the field today.

1. Development timing. Anchor everything to one date, the expected online date for the data center. Every other answer is graded against whether it can land by that date.

2. Land.

Is the land secured (ownership, lease, or option)?

Expected purchase price.

Acres available for development.

Flood, hurricane, or tornado risk zones.

Zoned for data center use.

Right-of-way permits or easements required to bring resources to the site.

Driving distance to key urban hubs.

3. Power (electricity).

Megawatts available today.

Expected online date for power if not yet available.

Existing electrical infrastructure on or near the site (substations, transmission lines).

4. Fiber.

Existing fiber connections on site.

Nearby fiber providers and approximate distance to connect.

Fiber density of key providers in the area.

Expected timeline to fiber connectivity.

Fiber routes from the site (which cities reachable, with what latency).

Fiber is fatal if missing. Without sufficient lit fiber to multiple major hubs, no hyperscaler will lease the data center, which means no off-taker for the energy plant. The site dies on this criterion alone.

5. Water.

Millions of gallons per day available.

Source mix: groundwater, surface water, or third-party providers.

If additional water is required, are the permits secured.

6. Gas.

Megawatts of prime power the site can support given current gas capacity.

Whether development work is required to bring gas to the site (lateral build, header tap).

Gas provider and expected gas price.

Proposed generation technology (turbine class, simple or combined cycle).

Timeline to install generation.

Whether emissions permits are secured for a prime power solution.

Why it matters

A great site solves 80% of the rest of the project. The wrong site multiplies every downstream problem. Recent examples: Pittsylvania County, Virginia killed a hyperscale gas project at the rezoning stage in 2025, costing $500M+ in foregone investment. Montour County, Pennsylvania rejected a co-location rezoning the same year. ERCOT projects in Pecos County have unlocked the Permian gas advantage for projects that picked the right basin proximity. The site decides what's possible.

Interdependencies

Site selection feeds every other decision. Air permit pathway is determined by airshed, attainment status, and proximity to environmental justice communities. Gas access is set by basin proximity and existing pipeline laterals. Water decides cooling design. Power and fiber decide whether a hyperscale tenant can use the site at all. Land control is the gating event for every permit application.

Risk

Binary on each of the six dimensions. Magnitude: any single missing piece is fatal. Mitigation: run the full six-dimension intake checklist in parallel for every candidate site before any capital deploys. This is the entitlement-first approach.

Underwriting impact

Site control is the gate that unlocks development capital. Without it, no lender or sponsor commits real money. Dev capital deployed before site control is fully at risk and rarely recoverable.

A 1 GW gas plant emits enough nitrogen oxides, carbon monoxide, and other pollutants to trigger Prevention of Significant Deterioration (PSD) Major Source review under the Clean Air Act. PSD requires a Best Available Control Technology (BACT) determination, an air quality impact analysis, and a public comment period. Once the air permit is issued, the plant also needs a Title V Operating Permit. State agencies run the process: TCEQ in Texas, Ohio EPA in Ohio, PA DEP in Pennsylvania.

Why it matters

Air permits are the single most likely point of total project failure. Best case for a 1 GW plant is 18-30 months. Worst case is 36-60+ months when community opposition or environmental justice review extends the process. xAI Memphis ran for months with 35 unpermitted gas turbines and faced a NAACP lawsuit before getting a permit for only 15 of them. Meta Apollo in Ohio used the OPSB expedited "letter of notification" pathway to compress to ~18 months. The permit is binary, it issues, or the project dies.

Modular strategy

Some projects break the plant into 200-300 MW modules under minor source NSR, which permits in 6-12 months per module. VoltaGrid's QPac platform has done this with stackable reciprocating engines. The catch: TCEQ and Ohio EPA aggregate emissions across modules at a single site if they share infrastructure, which kicks the project back to major source. Legal review before committing to this path is non-optional.

Interdependencies

Air permit timing drives NTP (no construction without permit), which drives EPC mobilization, which drives construction financing close, which drives first power. A 12-month permit slip slides every one of these by 12 months.

Risk

Binary. Magnitude: project-ending if denied. Mitigation: entitlement-first site selection, early community engagement, low-NOx burner specs at filing, third-party air quality baseline studies. Environmental justice screening (EPA's EJScreen) within a 3-mile radius can add 6-18 months.

Underwriting impact

Lenders will not close construction financing without a final, non-appealable air permit. Dev capital deployed before permit issuance is at full risk.

A 1 GW combined cycle plant burns roughly 150,000 MMBtu per day at full output, about 150 million cubic feet of gas a day. The gas has to come from somewhere, interstate pipeline, intrastate pipeline, or a new lateral built off a nearby header. Firm transport contracts (not interruptible) are required so the plant doesn't get cut off in winter.

Why it matters

A gas plant without firm gas is a paperweight. ERCOT projects sit on top of cheap Permian, Eagle Ford, and Haynesville gas, Pacifico's 7.65 GW GW Ranch in Pecos County could consume 1-2 Bcf per day, equivalent to 4-7% of 2025 Permian production. PJM projects in Ohio and Pennsylvania sit on top of Marcellus and Utica. Both basins are abundant, but pipeline expansion to a specific site can take 18-36 months and one easement holder can stop the whole project. TC Energy's open season in late 2025 for 1.2+ Bcf/d of Ohio capacity drew immediate hyperscale interest.

Interdependencies

Gas access is part of site selection. The plant's heat rate and capacity payment economics assume firm gas at a specific price. If the lateral build slips, plant COD slips. If the gas contract is interruptible instead of firm, lenders will not size the debt to peak output.

Risk

Continuous on lateral build (timing and cost), binary on easement holdouts. Magnitude: 12-24 month delay if a major pipeline component slips, $50-200M cost adders. Mitigation: select sites with existing pipeline access in place, sign firm transport contracts at financial close, build in redundant header connections where possible.

Underwriting impact

Lenders model gas cost as a pass-through under tolling agreements (off-taker pays fuel) but require firm transport to be in place at financial close. Gas price volatility itself is not the project's risk, the off-taker eats it. The risk is physical delivery.

Major US pipeline operators in the relevant corridors

Williams (Transco) operates the largest US gas pipeline system, with multiple expansions across Marcellus-to-mid-Atlantic and Gulf Coast corridors. Energy Transfer is the dominant Permian and Gulf Coast intrastate operator. Kinder Morgan operates Permian Highway and Gulf Coast Express plus brownfield expansions in DC-tied corridors. TC Energy ran an active 1.2+ Bcf/d Ohio open season for Marcellus/Utica-to-PJM throughput and is developing the NEXUS pipeline expansion path. Adjacent gathering, processing, and storage operators (MPLX, Enbridge, Boardwalk, Columbia Gulf) round out the relevant infrastructure stack. Industry trackers (East Daley, Arbo/NGI, INGAA) identify ~3-6 Bcf/d as the credible DC-tied pipeline range through 2028, growing to ~5-8 Bcf/d realistically when intra-basin gathering and pre-FERC announced projects are included.

A gas turbine takes in air, mixes it with gas, burns it, and spins a shaft that drives a generator. Three classes matter for a 1 GW project. Aero turbines (GE LM6000, LM2500) are derived from jet engines, small, fast-ramping, expensive per kW, used for peaking. F-class turbines (GE 7F, Mitsubishi M501F, Siemens SGT-750) are mid-range workhorses, 45-50% efficient in combined cycle. H-class turbines (GE 7HA, Mitsubishi M501JAC, Siemens SGT5-9000HL) are the largest and most efficient, 50-64% in combined cycle, lower NOx, hydrogen-ready, and the default choice for new 1 GW builds.

Why it matters

Lead times for new H-class orders are now 5-7 years. GE Vernova has 80 GW of backlog plus reservation agreements as of end-2025. Siemens Energy is sold out through 2030. Mitsubishi is sold out through 2028. Reservation deposits, paying just to hold a delivery slot, are now $50-150M per unit and 10-20% of capex. For a 1 GW project (typically 9 H-class units in combined cycle) that's $500M-$1.5B in deposits before construction starts.

Modular reciprocating fallback

Because H-class lead times are so long, fast-deploy projects use modular reciprocating engines (Wärtsilä, Caterpillar, INNIO) for first power. Oracle Shackelford uses 210 industrial gas generators on the VoltaGrid platform. Meta El Paso uses 366 MW of modular Caterpillar units. xAI Memphis runs 27 turbines in a modular configuration. These are smaller per unit but stackable, deploy in months instead of years, and bridge the timeline until H-class arrives for the combined cycle phase.

Interdependencies

Turbine selection drives air permit content (BACT depends on the chosen technology), plant footprint, gas demand, water demand, and capex. The order date drives delivery, which drives mechanical completion, which drives first fire and COD.

Risk

Continuous on lead time and price, binary on OEM solvency or geopolitical disruption. Magnitude: 12-36 month delay if OEM allocation slips, $100M+ capex variance.

Underwriting impact

Lenders require executed equipment contracts and paid deposits before construction financing close. Late-cycle slot-poaching (buying someone else's reservation at a markup) is now a real cost line.

A Battery Energy Storage System sits between the power plant and the data center load. It absorbs sub-second power swings that the gas turbines cannot follow. Lithium-ion is the standard chemistry. For a 1 GW AI campus, sizing typically falls in the 100-500 MWh range, costing $300-600 per kWh, or $150-300M for a 500 MWh system.

Why it matters

AI training workloads are nothing like traditional data center loads. During checkpointing, the periodic save-state of a training run, power demand can swing by 20-50% of peak in seconds. H-class gas turbines ramp at 10-20 MW/min. They cannot follow a 500 MW spike that arrives in under a second. Without BESS, grid frequency drops, the plant trips, the training run dies. BESS bridges the gap. Some campuses also add supercapacitors for the fastest transients (under 100 ms), with the BESS handling 1-10 minute smoothing and the turbines handling sustained load.

Interdependencies

BESS sizing depends on training workload profile (talked through with the hyperscaler at lease design), turbine ramp capability, and whether the plant runs islanded. Black start capability also depends on BESS being charged. BESS placement (data center side vs plant side) affects interconnection and metering.

Risk

Continuous on cost, supply chain, and degradation. Lithium-ion BESS lose roughly 2% capacity per year and need replacement at 10-15 years. Magnitude: under-sized BESS results in plant trips and lost compute revenue; over-sized BESS is wasted capex.

Underwriting impact

BESS is line-itemed in the project capex budget. Lenders treat BESS as integrated infrastructure for behind-the-meter projects. In PJM, BESS qualifies for capacity payments where standalone gas behind-the-meter does not, making BESS placement a revenue-stack decision, not just a technical one.

Black start is the ability to start the power plant from zero, no help from the grid, no outside power. A small synchronous generator (typically 50-100 MW, sometimes a diesel set, sometimes an aero turbine) fires up, stabilizes voltage and frequency on the local island, then starts the larger gas turbines and BESS. Once the plant is humming, it can carry the data center load.

Why it matters

Behind-the-meter data centers run islanded for years before grid interconnect comes online. If the plant trips during operation, equipment failure, fuel disruption, weather, there is no grid to fall back on. Black start is the only way to recover. For the reference project, the plant runs BTM from 2028 to 2032, four years where black start is the only recovery path. Once grid backstop is live, the grid can do the work, but black start capability typically stays in place as a redundancy.

Interdependencies

Black start design integrates with BESS (used to stabilize during ramping), control systems (the sequence has to be modeled and validated), and EPC scope (the small starter set is procured and commissioned alongside the main equipment). Validation simulations typically take 3-6 months.

Risk

Continuous on design and validation. Magnitude: small in capex terms (well under 5% of plant cost) but binary on operational risk, without it, a single trip can take the data center offline for hours or days. Siemens Energy won the first US black-start battery storage project in 2025.

Underwriting impact

Lenders require demonstrated black start capability for any BTM project before construction financing close. It's a checklist item but a non-waivable one.

A gas-fired power plant runs in one of two modes. Simple cycle (also called open cycle) burns gas in a turbine, spins a generator, and vents the exhaust. Combined cycle adds a heat recovery steam generator that captures the exhaust heat to drive a steam turbine, the same fuel produces 30-40% more electricity. Simple cycle is 35-40% efficient. Combined cycle is 50-64% efficient.

Why it matters

Simple cycle is faster to build (18-24 months) and cheaper per kW ($600-900). Combined cycle takes 36-48 months and costs more ($800-1,200 per kW, plus the steam cycle adds another $300-500 per kW), but burns about a third less gas for the same power. For a 1 GW plant running base load, combined cycle saves enough on fuel to pay for itself many times over its life. The dominant 1 GW pattern for hyperscale: simple cycle for first power, then add the steam cycle on top. This gets first MW to the data center 18-24 months earlier and lets the steam tail come online once the combined cycle equipment arrives.

Interdependencies

Plant configuration drives air permit emissions profile (combined cycle has lower per-MWh emissions, easier BACT), water demand (combined cycle needs more cooling water for the steam loop), capex profile (phased), turbine selection (H-class preferred for combined cycle), and project timeline.

Risk

Mixed. Simple cycle alone leaves efficiency on the table for a base-load hyperscale tenant. Combined cycle alone delays first power. Phased build is the dominant pattern but adds construction sequencing complexity. Magnitude: choosing wrong adds 18-24 months or 30%+ to lifetime fuel cost.

Underwriting impact

Phased build allows phased financing, Phase 1 simple cycle gets to revenue faster, supporting Phase 2 combined cycle financing. Modular reciprocating engines are an even faster Phase 1 alternative when H-class lead times bind.

EPC stands for Engineering, Procurement, and Construction. The EPC contractor designs the plant, buys the equipment, and builds it. Major firms in the hyperscale + power space: Bechtel, Kiewit, Fluor, Black & Veatch, Burns & McDonnell. Bechtel and Kiewit are working together on the $33B Ohio PORTS project. Kiewit is building Homer City's record 4.5 GW gas plant in Pennsylvania.

Why it matters

Two things are true at once. First, the major EPCs are oversubscribed, 12-18 month delays just to lock an EPC selection in 2026. Second, US craft labor is short by 350,000-500,000 workers nationally, with electricians, pipefitters, welders, and HVAC techs the most constrained. Even with money, permits, and equipment, finding the people to build the plant can add 6-12 months. Wage premiums are 10-25% above 2024 baselines for critical trades.

Contract structures

Pure lump-sum turnkey (LSTK) is dying. EPCs will not absorb full cost and schedule risk on megaprojects in this market. Hybrid structures dominate: phased lump-sum (LSTK on engineering and procurement, reimbursable on construction), target price with pain-gain (50/50 share above and below an agreed cost target), or EPCM where the EPC manages but the owner carries direct labor and material costs.

Interdependencies

EPC contract type drives risk allocation across the project and how lenders size construction debt. EPC mobilization depends on long-lead procurement (turbines, switchgear) being secured. EPC labor competes with every other megaproject in the region.

Risk

Continuous on schedule, cost, and labor. Magnitude: 6-12 months on labor, $50-200M on cost overruns at the project scale. Mitigation: lock EPC early (12-18 months pre-NTP), pre-negotiate craft labor agreements, use modular prefabrication where possible.

Underwriting impact

Lenders require executed EPC contract before construction financing close. Hybrid structures require larger contingency reserves (10-15% vs 5-8% for true LSTK). Owner-side cost risk has shifted up.

The off-take agreement is the contract between the power plant and the data center tenant. It comes in two main forms. A Power Purchase Agreement (PPA) sells energy at a fixed or indexed price. A tolling agreement charges a fixed capacity payment plus pass-through fuel, the off-taker provides the gas, the plant converts it. For behind-the-meter co-located projects, tolling is preferred because it aligns the tenant's fuel risk with their compute economics.

Why it matters

The off-take agreement is the project. Without a 15-20 year credit-backed contract to an investment-grade tenant, the project does not get financed. An IG-rated hyperscaler (Google, Meta, AWS, Microsoft) enables 60-65% project debt. Sub-IG counterparties cut leverage to 45-55% and require parent guarantees or letters of credit equal to 12-24 months of fixed payments. Non-rated counterparties typically cannot finance project debt at all without third-party credit support.

Term mismatch problem

A typical hyperscale data center build-to-suit lease runs 15 years. A typical gas plant PPA runs 20 years. When they don't match, the project hits a refinancing cliff at year 15, the lease expires, the energy debt still has 5 years to run, and lender collateral value drops 30-50%. Three solutions exist: extend the DC lease to 20 years (most common today), separate the financing books for DC and energy, or pool both into a single tranched ABS. None is dominant; the market is still solving this. Underlying issue: residual value beyond the initial lease period is speculative in frontier markets at hyperscale (no proven re-leasing market at GW scale outside core hubs). See Deep Dive 11 for the residual value debate, the disciplined position is to underwrite IRR within the initial lease and treat residual as upside, especially in frontier markets.

Interdependencies

Off-take credit drives debt sizing on both DC and energy. Off-take tenor must match financing tenor. Off-take volume commitment ("all-or-nearly-all" 90-95% capacity) drives revenue certainty. Take-or-pay floors protect against tenant ramp delays.

Risk

Cliff risk. Off-taker default is low probability with IG tenants but project-ending if it hits. Magnitude: full project at risk. Mitigation: term matching, parent guarantees, take-or-pay minimums, standby letters of credit.

Underwriting impact

Off-take credit IS the energy project debt collateral, not the plant. The plant has no merchant market in BTM mode; if the tenant exits, the asset is stranded. Off-taker credit quality cascades across all three stakeholders (DC developer, hyperscaler, energy developer) and is the central link enabling each party to size debt against the same counterparty. See Deep Dive 30 for how off-take credit feeds into cross-stakeholder capital optimization.

The capital stack is who puts money in and on what terms. For a 1 GW gas plant under tolling agreement, the typical stack is 30-40% sponsor equity, 55-65% senior secured project debt, and (rarely) 0-10% mezzanine. Debt tenor matches PPA tenor, 15-20 years. Senior debt is sized to a minimum debt service coverage ratio (DSCR) of 1.30-1.40x. Tolling structures get slightly more aggressive sizing (1.25-1.30x) because off-taker credit absorbs fuel and dispatch risk.

Why it matters

The numbers determine what's possible. Energy infra: unlevered IRR on a stabilized tolling plant with an IG off-taker runs 8-12%. Levered IRR for sponsor equity runs 14-18%. DC developer: hyperscale build-to-suit development IRRs run 25-40% during the dev period (3-4 year hold), stepping down to 8-10% at stabilization, with stack of 25-35% sponsor equity, 50-60% construction debt, replaced by 50-60% LTV permanent debt at COD. Recent comps support these ranges: Macquarie put $112.5M of preferred equity into Applied Digital's Polaris Forge alongside $277.5M of APLD sponsor equity, implying ~40% blended equity and ~60% debt.

Sub-IG impact

Investment-grade off-take enables max leverage. Sub-IG cuts sponsor equity from 30% to 40-45% and adds 150-250 bps to all-in cost of capital.

The residual value debate

A real point of commercial tension that the doc should not duck: should DC developers underwrite the lease to deliver target return in the initial lease period (15 years), or rely on residual value (renewal, sale, repurpose) to hit the IRR? Two views in market.

The traditional view, residual is real. Hyperscale build-to-suit reaches stabilization in 3-4 years (developer-flip exit captures 25-40% dev IRR), and long-term holders earn 9-11% YoC over 9-11 years (full cash payback). Re-leasing markets in core hubs (Northern Virginia, Dallas, Phoenix) support 80-90% of original rent on renewal. Underwriting to residual is defensible.

The disciplined view, residual is speculation in frontier markets. At gigawatt scale in West Texas, Wyoming, the Permian, or rural ERCOT, there is no proven re-leasing market. If the hyperscaler walks at year 15, the asset sits idle. The right target is to deliver the IRR in the initial lease period and treat residual as upside, not baseline. This pushes minimum YoC at frontier sites to 9.5-10.5% rather than the 8-9% being accepted in some recent deals. Lower yields on frontier mega-sites ride on the assumption that hyperscale demand will persist beyond the initial lease, and that's not a contracted assumption.

The energy developer's logic applies: never underwrite to a merchant tail you don't control. Same principle should govern DC underwriting in markets without proven secondary demand. Core markets with IG triple-net off-take can defensibly accept lower YoC because the residual is real. Frontier sites at scale cannot. The recent industry pattern of accepting 8-9% YoC at frontier mega-sites is taking on more residual risk than the underlying market has proven out.

Interdependencies

Off-take credit drives debt sizing. EPC contract type drives contingency reserves. Permits drive financial close timing. Turbine deposits eat working capital before debt is even drawn.

Risk

Mixed. Underwriting risk lives in the assumptions, DSCR holds only if revenue holds, which holds only if off-taker performs.

Underwriting impact

Lenders model 15-20 year base case with stress scenarios on heat rate, availability, and off-taker ramp delays. Construction debt rolls to permanent at COD; mini-perm structures (5-7 year tenor with refinance) are common as a bridge.

Conditions precedent (CPs) and project-on-project risk

The underlying problem is a 3-year capital gap before bankability. Firm transport precedent agreements and turbine reservation deposits ($600M to $2B for a 1 GW project) typically have to be committed 24 to 36 months before a hyperscaler PPA can be executed. Project finance debt cannot fund any of this because lenders require an investment-grade off-take commitment to size construction debt. The result is that dev-stage capital is 100% at-risk equity for 24 to 36 months. The CPs below are the standard list lenders use to test whether the project is ready to close; the mitigation toolkit further down is the standard toolkit sponsors use to manage the dev-stage capital exposure.

Energy project finance closes only when a defined list of CPs are all satisfied. Standard CPs for a 1 GW gas plant:

Final and non-appealable air permit (PSD major source or minor source NSR)

Executed EPC contract with bonding and warranties from a Tier 1 contractor

Executed PPA or tolling agreement with an investment-grade off-taker

Executed gas supply agreement

Executed firm transport agreement (or precedent agreement with a major pipeline)

Turbine reservation deposits paid; mechanical completion date secured

Generator interconnection agreement (where required for first power, see Deep Dive 23)

Land control documents (deed or long-term lease)

All material regulatory approvals (water, county/state environmental, FERC, other)

Sponsor equity committed and funded into escrow

Insurance bound (construction all-risk, delayed startup, marine cargo where applicable)

Independent engineer report and lender's technical advisor sign-off

Each CP is binary. Missing one delays financial close, which delays construction debt, which delays NTP, which delays first power.

When the energy plant and the data center are co-located but separately financed, each side's CP chain depends on the other side's progress. The energy plant cannot close without an investment-grade off-taker (the DC tenant). The DC cannot commit to a fixed compute-online date without certified power delivery (the energy plant). Both CP chains have to land in parallel, and a slip on either side cascades. This is the project-on-project risk.

Specific cascading failure modes:

DC tenant pushback on PPA price reduces off-take credit, which reduces energy debt size, which opens a sponsor equity gap and stalls the project.

Air permit appeal at 11 months into the issue period misses the CP; financial close slips 6-12 months; construction debt rolls; interest carry escalates; IRR compresses.

Turbine order cancelled by sponsor (or OEM defaults on delivery date) eliminates mechanical completion; NTP cannot be issued; the DC tenant declares MAC under the offtake agreement.

Mitigation structures. The market has developed a toolkit for managing project-on-project risk: parent guarantees from the hyperscale tenant covering specific obligations; take-or-pay PPAs with damage payments scaled to construction milestones; hyperscaler funding of dev capital (Google/Intersect template at $4.75B); equipment lease structures (Halliburton/INNIO 2.3 GW); escalating LCs at milestones (3-month, 6-month, 12-month); defined-event acceleration clauses with damage payments; completion and performance insurance (limited market, expensive).

Sponsors with strong hyperscaler relationships can shift project-on-project risk back onto the tenant. Sponsors without that leverage carry the risk themselves and price it into IRR targets. Integrated platforms (energy + DC under one sponsor) eliminate project-on-project risk by definition, which is part of why the market is consolidating in that direction. These mitigation structures are practical expressions of the cross-stakeholder capital optimization framework in Deep Dive 30: each is moving a specific risk to the party with lowest cost of bearing it, given their different capital costs and time horizons.

Capital does not arrive all at once. It is released against project milestones. A 1 GW co-located project moves through five financing stages: development capital (5-10% of total cost) for site, entitlements, design, and financing fees; bridge facility for early procurement; construction debt (50-60% of total cost) drawn against hard cost milestones; mini-perm or permanent debt at COD; and refinancing once the asset is stabilized.

Why it matters

Each stage is a separate risk hurdle and a separate financing event. Site control unlocks dev capital. Air permit + executed PPA + executed EPC unlock construction financing close. NTP releases construction debt against drawdowns. Mechanical complete and first fire trigger the next tranche. COD converts construction debt to permanent debt. If any gate slips, the next tranche is held.

Dev capital reality

Dev capital is fully at risk until financial close. For a $2.5B 1 GW gas plant, dev capital is $125-250M held for 24-36 months with no return guarantee. Hyperscalers increasingly pre-fund or guarantee dev-capital reimbursement, which materially de-risks the sponsor, but this is a negotiated outcome, not a market default. This shift from sponsor-funded to hyperscaler-backed dev capital is a direct reflection of the different cost-of-capital across parties (sponsor at 15%+, hyperscaler at near-balance-sheet cost) and is the market's move toward the cross-stakeholder optimization framed in Deep Dive 30.

Promote structure

Sponsors capture upside through promote schedules: typical 15-25% of profits above an agreed hurdle IRR, sometimes with a stepped waterfall (e.g., 20% above 12% IRR, 30% above 18%). For integrated DC + energy projects, promote often covers the whole project on a blended basis.

Interdependencies

Stage-gating ties every other section together. Permits unlock finance unlocks NTP unlocks construction unlocks COD unlocks permanent debt unlocks promote. One stuck gate stops everything.

Risk

Continuous on dev-capital exposure (long timeline, full at risk), binary at each gate (financial close happens or doesn't).

Underwriting impact

Lenders model the full waterfall. Sponsors model the dev-capital deployment curve and the equity check size at each gate.

Risks come in three shapes. Binary risks either pass or kill the project, air permit issued or not, FERC interconnection approved or not, off-taker investment grade or not. Continuous risks can be managed with time and money but always cost something, turbine delivery slip, gas pipeline build, EPC labor shortage, weather. Cliff risks are low probability but project-ending if they hit, off-taker default, EPC default, fuel supply default, regulatory rule change.

Why it matters

Each risk shape needs a different mitigation strategy. Binary risks demand entitlement-first selection (only sites and counterparties that pass). Continuous risks demand contingency time, contingency budget, and parallel paths. Cliff risks demand contractual protections (parent guarantees, LCs, take-or-pay, force majeure provisions).

Magnitude scale

For the reference project: binary risks risk the entire $2.5B+ project. Continuous risks typically cost 5-20% of project budget and 6-18 months of schedule when they materialize. Cliff risks vary, off-taker default is full project loss; EPC default can be replaced (with a 12-24 month delay and 10-20% cost adder).

Risks by stage

Site & Land: binary site control, continuous due diligence findings

Permits: binary air permit, continuous local pushback timeline

Lenders price binary risks as conditions precedent to close (the risk is gone before debt is drawn). Continuous risks are absorbed in contingency reserves and base-case stress tests. Cliff risks require contractual structures, usually parent guarantees, security deposits, or take-or-pay floors.

Sources: Synthesizes risk frameworks from project finance literature, Morgan Lewis, S&P Global, NREL ATB methodology referenced throughout this guide.

14, Regional Comparison: ERCOT vs PJM

ERCOT (Texas)

Speed to power: fastest in the US. Median 4.1 years in queue for batteries; 2.5 years from interconnection agreement to operation. Senate Bill 6 (June 2025) and the upcoming Batch Study process (proposed Feb 2026) add structure but also new disclosure and curtailment rules.

Capacity market: energy-only. There are no capacity payments. Plant revenue depends entirely on volatile real-time energy prices, which lenders penalize.

Behind-the-meter: SB 6 allows BTM if generation is non-exporting and ≥50% of demand is on-site. Generators majority-owned by the load customer's parent as of January 1, 2025 are exempt from co-location review.

Gas access: excellent. Permian, Eagle Ford, Haynesville. 40 GW of gas projects planned to power Texas data centers.

Permitting: TCEQ air permits run 3-6 months for minor source, 18-36 months for major source. Water is the emerging constraint, TCEQ now reviews any project >5 MW.

Tax: JETI program offers 100% school M&O abatement during construction, 50% in operations, sunsetting 2033.

Community climate: state-supportive but local opposition rising. Public polling shows 80% support for taxing AI data center electricity.

PJM (Ohio and Pennsylvania)

Speed to power: historically 4-8 years; reformed rules promise 1-2 years for projects entering Cycle 1 in spring 2026. Backlog of 195 GW still working through.

Capacity market: RPM auction provides predictable revenue. The 2026/27 and 2027/28 auctions cleared at the price cap ($329 and $333 per MW-day). This is a real second revenue stream for new gas, significantly improves financing.

Co-location rules: FERC's December 2025 order directed PJM to reform its tariff for co-located generation by January 2026, with partial acceptance in April 2026. The framework is still settling.

Gas access: Marcellus and Utica. TC Energy's Ohio open season covers 1.2+ Bcf/d. Pipeline expansion timelines run 2-4 years.

Permitting (Ohio): Ohio EPA + OPSB expedited "letter of notification" path. Meta Apollo (350 MW Wood County) compressed to ~18 months. No state property tax on equipment.

Permitting (Pennsylvania): PA DEP, similar timelines to Ohio. But 68% of PA voters oppose data centers in their neighborhood. Montour County rejected co-location rezoning in 2025.

Tax (Ohio): sales tax exemption with $100M investment threshold, no personal property tax.

Tax (PA): sales exemption exists but is under repeal threat by the Shapiro administration.

Community climate: Ohio is pro-business and supportive. PA is the most politically difficult market in the US for new gas-fired hyperscale.

Bottom line

ERCOT wins on speed to power. PJM Ohio wins on financing certainty (capacity market) and tax. PA carries the most political risk. The 1 GW reference project in ERCOT is fastest but trades capacity revenue for energy-only volatility. Same project in PJM Ohio takes longer but finances more cleanly. The right choice depends on which is the binding constraint, speed or capital cost.

More than $300B was committed across hyperscale DC + dedicated power deals in the 12 months from May 2025 to May 2026. Three patterns dominate.

Pattern 1: Behind-the-meter for speed

Oracle Shackelford runs 700 MW pure off-grid via 210 modular generators on the VoltaGrid platform. xAI Colossus runs 1.2-2 GW behind-the-meter from 27+ gas turbines. Meta El Paso uses 366 MW of modular Caterpillar units. Project Baccara in Phoenix runs 700 MW off-grid for two 1M-square-foot data centers. These projects bypass the ERCOT or PJM queue entirely. First power 2027-2028. They sacrifice grid capacity revenue for time.

Pattern 2: Utility partnership for scale

Meta Richland Parish co-developed 2,200 MW of dedicated Entergy gas turbines ($3.2B utility + $10B+ Meta DC). Compass Datacenters Mississippi with Mississippi Power for a 500+ MW $10B campus. Full capacity-market integration but slower (2028-2029).

Pattern 3: Nuclear for decarbonization

Microsoft-Constellation 20-year 835 MW Three Mile Island restart, accelerated to 2027 with $1B DOE loan. Amazon-Talen $18B 1.9 GW Susquehanna, transitioning to "front-of-meter" spring 2026 after FERC scrutiny. Google-TVA-Kairos 50 MW SMR with load-limiting agreements.

Implications for the reference project

A 1 GW gas + 1 GW DC co-located build in ERCOT is the most replicable pattern. It combines Pattern 1 (modular gas BTM for fast Phase 1 to 2028) with combined cycle for full 1 GW by 2031, plus grid backstop in 2032.

A hyperscale data center is a large industrial building with raised floor or slab, mechanical infrastructure for cooling, IT equipment racks (servers, switches, GPUs), power distribution gear, fiber connectivity, and physical security. Build-to-suit for a hyperscaler runs 12-24 months from greenlight to operational if the site is de-risked, power secured, fiber lit, permits in hand. Capex for a 1 GW DC campus runs $4-7B depending on cooling architecture and IT spec.

Why it matters

The DC is the off-taker. The energy plant exists to serve it. If the DC can't come online when the hyperscaler needs it, the energy plant has no customer. The DC's clock and the energy plant's clock are not naturally aligned, that mismatch is the central problem of the integrated model (see Section 17).

Cooling drives everything

Current hyperscale practice for AI training is direct-to-chip liquid cooling, with PUE targets 1.10-1.12 and water usage targets <0.30 L/kWh (Microsoft). New builds are testing closed-loop immersion to eliminate water dependency, at higher cooling capex.

Interdependencies

DC site is shared with the energy plant. Power dependency drives the timeline. Fiber dependency is fatal if missing. IT equipment lead times (GPUs, switchgear, transformers) compete with every other hyperscale project. Lease execution is the binary gate that unlocks DC construction financing.

Risk

Continuous on schedule and IT equipment delivery. Binary on tenant lease execution. Cliff on tenant exit.

Underwriting impact

DC build-to-suit dev IRR 25-40% over 3-4 year hold, stepping down to 8-10% stabilized. The same hyperscaler IG credit drives both DC lease and energy PPA, sub-IG cuts leverage on both sides. The credit quality cascade across all three stakeholders (DC developer, hyperscaler, energy developer) is one of the central coordination points in the cross-stakeholder capital optimization framework (Deep Dive 30).

The full Digital Master document treats DC development as its own subject. This section is the overlay summary needed to make the Energy Master complete.

The structural mismatch between when the data center is ready to come online and when the gas-fired energy plant can deliver firm full power. In the reference project, the DC could be physically built by 2027 (12-18 months from go), but the gas plant doesn't hit full 1 GW until 2031. The gap is roughly 3 years.

Why it matters

Hyperscalers do not sign 15-20 year leases without firm power on a date they can plan around. Energy developers do not commit dev capital without a signed PPA. The two parties stand on opposite sides of a chicken-and-egg problem. Without a coordination mechanism, no project happens.

Three approaches, what each actually does, what each doesn't

None of these three fully closes the gap. Read them as contrasts to the reference example, not as solutions.

Phased ramp with modular gas. Modular reciprocating engines (Wärtsilä, Caterpillar, INNIO) deliver 250-500 MW in months from NTP. H-class combined cycle arrives 5-7 years later for full 1 GW. The DC ramps load as power becomes available. Examples: Oracle Shackelford, Meta El Paso, xAI Memphis. This is the dominant near-term strategy for compressing the physical timeline to compute (alternatives in Deep Dive 22). It buys 18-24 months on first MW. It does not eliminate the wait for full power.

Hyperscaler vertical integration. The hyperscaler buys or co-develops the power source. Google's ~$4.75B acquisition of Intersect Power's digital power assets (reported December 2025; verify exact terms before any external use) is the canonical example. This does not compress the build timeline. Owning the power developer doesn't make air permits issue faster, doesn't shorten turbine lead times, doesn't build pipelines quicker. What it does: removes the chicken-and-egg counterparty problem, captures all power margin internally, provides delivery certainty. The hyperscaler still waits 4-5 years for full power.

Utility partnership. Regulated utility builds the plant under its own ratebase, hyperscaler is anchor customer. Meta Richland Parish with Entergy ($3.2B utility capex, $10B+ Meta DC). Also does not compress the build. What it does: provides regulated-utility credit (improves project financing), captures capacity market revenue (in PJM), and shifts development risk onto the utility ratebase. Slower to first power than phased modular gas. Better long-term economics than greenfield project finance.

The honest synthesis. Only phased modular gas actually moves the physical timeline. The other two strategies are valuable for different reasons, coordination, financing, risk shift, but they don't shorten the wait. The 3-year gap is structural. It comes from permits, pipelines, turbines, and EPC labor. Ownership structure and counterparty arrangement don't change the physics.

Interdependencies

The bridge chosen determines PPA timing, lease timing, capital sequencing, and risk allocation. Phased ramp keeps the energy developer at maximum risk. Vertical integration shifts risk to the hyperscaler. Utility partnership shifts risk to ratepayers.

Risk

Mixed. Binary on whether the gap is closed before either party walks. Continuous on cost of bridging. Cliff on tenant ramp delay if the bridge is fragile.

Underwriting impact

The gap creates a refinancing cliff if the bridge is not term-matched. Lenders model the ramp explicitly, a phased ramp project must show committed off-take volume escalation matched to plant phasing, with take-or-pay floors to protect against DC ramp delays.

Phased ramp is the only approach that actually compresses physical time. Section 18 (BTM Acceleration) is the deep dive on what that looks like in practice.

18, BTM Acceleration · The Path Everyone Is Taking

What it is

Behind-the-meter (BTM) modular gas. Reciprocating engines from Wärtsilä, Caterpillar, INNIO, deployed via integrator platforms (VoltaGrid QPac, TECO Westinghouse, Halliburton/INNIO partnership, Caterpillar Energy Solutions). Engines are 1-20 MW per unit. Practical minor-source ceiling is around 500-700 MW per site, limited by air permit aggregation rules (<100 tons/yr criteria pollutant), which depend on engine technology (modern SCR + ox cat units have ~0.1-0.3 g/bhp-hr NOx vs ~0.5+ for older platforms), operational hour caps, and state regulator interpretation (TCEQ more permissive than Ohio EPA than PA DEP). Above 500-700 MW, BTM still works, projects accept PSD major source review, which adds 18-24+ months to the permit timeline but unlocks larger scale. Halliburton/INNIO's 2.3 GW manufacturing deal signals that >1 GW BTM is coming for projects willing to do PSD. Reference deployments: Oracle Shackelford (210 VoltaGrid generators, 700 MW, at the upper end of minor source), Meta El Paso (366 MW modular Caterpillar), xAI Memphis (27+ turbines), Project Baccara (700 MW). Run on natural gas at 35-42% thermal efficiency (simple-cycle equivalent). Fast ramp (0-100% in 7-10 seconds for Caterpillar).

Why it matters

This is the dominant near-term strategy that compresses physical time to first power. Traditional CCGT takes 4-7 years. BTM delivers 250-500 MW in 12-24 months from project go. Other accelerators exist (nuclear restart, SMRs, grid headroom arbitrage), but BTM is the most scalable per-site near-term play. See Deep Dive 22 for the alternatives sensitivity table. That is the answer to the 3-year disjointedness gap. Every major hyperscale project shipped in the last 18 months has used some form of BTM modular gas, either as a permanent solution (xAI, Project Baccara) or as Phase 1 bridge to CCGT (the dominant pattern, used by the reference project).

Realistic timeline, even temp power is long

Aggressive 12 months. Typical 18-24 months. Modular OEM lead times in 2026 are 9-18 months (Halliburton's 2.3 GW deal with INNIO is expanding manufacturing capacity through 2028). Minor source NSR air permits run 6-12 months when structured below aggregation thresholds. Site prep, gas tap, electrical interconnection, commissioning add 3-6 months.

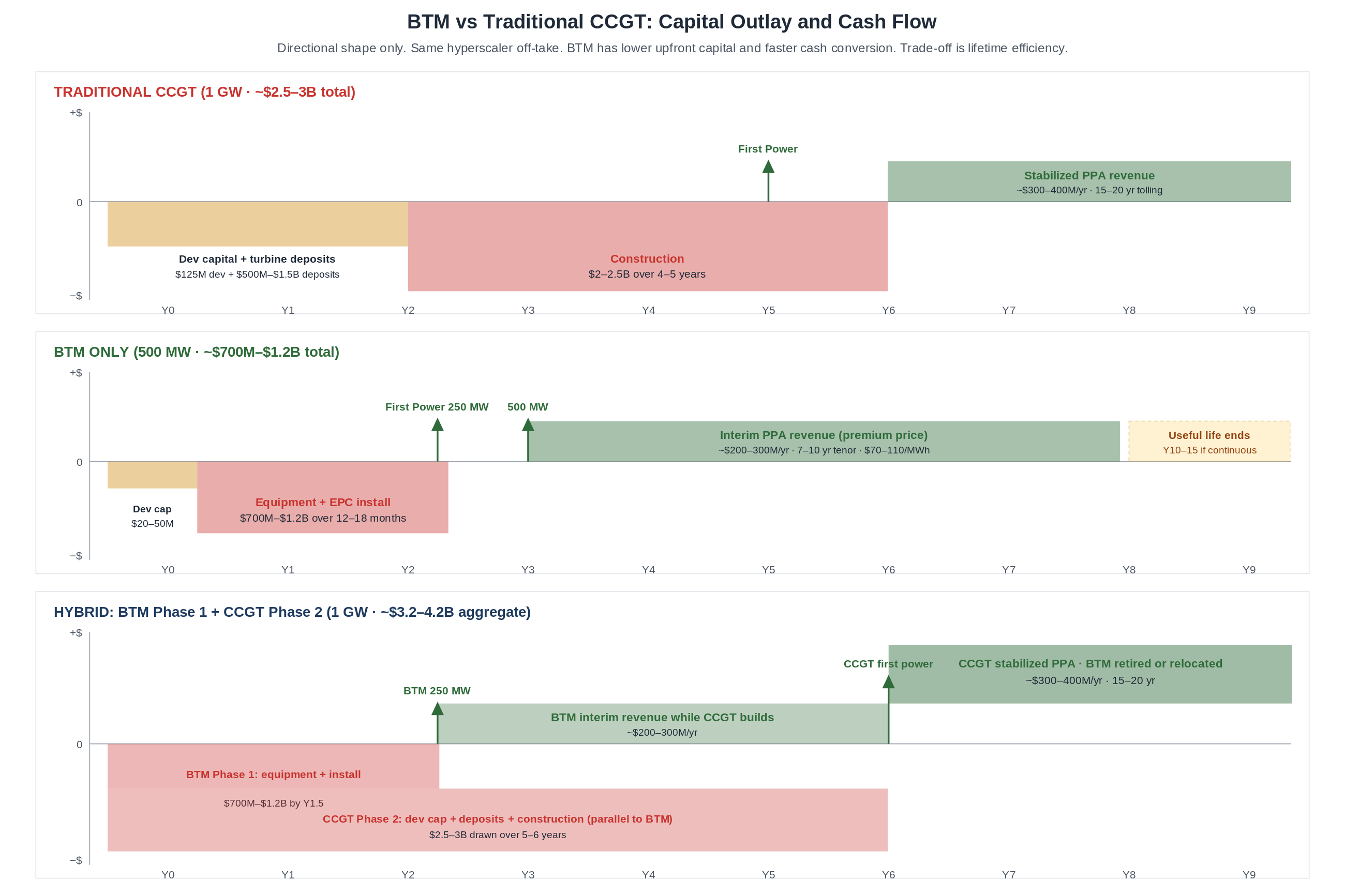

Capital outlay compression

Directional shape only. Same hyperscaler off-take. BTM has lower upfront capital and faster cash conversion. Trade-off is lifetime efficiency.

Traditional CCGT (1 GW): $125M dev capital + $500M-$1.5B turbine deposits committed in Y0-Y2, $2-2.5B construction draws Y2-Y6, total $2.5-3B before any revenue. First revenue Y5-Y7.

BTM Only (500 MW, minor-source typical): $20-50M dev capital + $700M-$1.2B equipment + EPC committed in Y0-Y1.5. First revenue Y1-Y2.

BTM Only (1 GW, PSD major source): ~$1.4-2.4B equipment + EPC, deployable in 30-48 months (12-24 mo build + 18-24 mo extra for PSD permit). Same per-kW economics, larger scale, longer permit.

Per kW first power: Traditional ~$2,500-3,000/kW for ~5 year wait. BTM ~$1,400-2,400/kW for ~1.5 year wait.

The backstop reality

No energy developer funds BTM without a backstop from the DC developer or hyperscaler. This is a project finance hard requirement. Four reasons: stranded asset risk (BTM has 10-15 year useful life; relocation costs $200-400/kW; secondary market is thin), limited useful life economics (35-42% thermal efficiency vs 50-64% for CCGT means 25-40% higher fuel cost per MWh), performance risk (90-93% availability vs 95-97% for CCGT), single-tenant exposure (no merchant tail).

Backstop structures actually used: hyperscaler balance-sheet capex (Google-Intersect model extended), interim PPA at premium price ($70-110/MWh vs $50-70/MWh for CCGT), take-or-pay covering 90%+ of capacity, letters of credit equal to 18-24 months of fixed payments, equipment lease structures (Halliburton/VoltaGrid 2.3 GW deal, Halliburton retains ownership, hyperscaler pays fixed lease rate), OEM manufacturer guarantee. Without one of these, no project finance lender will fund BTM development capital.

These backstop structures are functionally cross-stakeholder capital optimization in practice: each moves a specific risk to the party with the lowest cost of bearing it (usually the hyperscaler, which has lower cost of capital and direct control over offtake certainty) in exchange for hyperscaler upside on power-margin economics. Deep Dive 30 formalizes the framework that explains why these structures emerge in market.

Risk profile differs significantly from traditional

Risk dimension

Traditional CCGT

BTM Only

Hybrid

Air permit

PSD major (18-60+ mo)

Minor NSR (6-12 mo, aggregation risk)

Both

Equipment lead time

5-7 years

9-18 months

Both

Up-front capital at risk

$500M-$1.5B in deposits

$250-500M in equipment

$750M-$2B layered

Stranded asset risk

Low

High (limited life)

Medium

Performance availability

95-97%

90-93%

Mixed

Off-taker backstop

PPA standard

Interim PPA + backstop required

Both

Useful life

25-30 years

10-15 years (5-7 if bridging)

Mixed

Underwriting differs for both sides

Energy: PPA tenor 7-10 years vs 15-20, sponsor equity 40-50% vs 30-40%, debt premium 200-300 bps, DSCR 1.40-1.50x vs 1.30-1.40x, unlevered IRR 12-15% vs 8-12%. Often equipment-financed via OEM (60-70% of equipment capex via lease) or hyperscaler-funded via balance sheet (eliminates project finance entirely).

DC: Development IRR target unchanged at 25-40% but compute-online date moves up 3 years; same hyperscaler IG credit drives both sides; lease tenor may shrink to match BTM if no CCGT phase planned.

Hybrid is the dominant new-build pattern

BTM Phase 1 delivers first MW in 12-24 months. CCGT Phase 2 delivers full 1 GW by year 6-7. BTM gear retired or relocated as CCGT comes online. Reference project uses this. Combines speed (BTM) with long-term efficiency and credit (CCGT). Capital stack is layered, BTM financed separately (often as bridge facility or balance sheet), CCGT as long-term project finance. BTM's interim cash flows partially offset CCGT dev capital exposure.

Limitations

Practical minor-source ceiling 500-700 MW per site (above this, projects accept PSD major source review, adds 18-24+ months to permitting but no hard cap on scale). Higher fuel burn per MWh. OEM supply chain constrained. Stranded asset economics on relocation. Black start dependency (no grid fallback). Local pushback risk (xAI Memphis ran 35 unpermitted gas turbines, faced NAACP litigation).

What this means for the macro gap

BTM compresses one project's time to first compute. It does not solve the macro supply ceiling. Pipeline capacity (3-4 Bcf/d announced expansion through 2028), modular OEM capacity, air permit aggregation, and stranded asset economics still cap how much BTM the market can absorb. BTM is essential for individual projects. It is not a solution for the industry.

See also: standalone BTM_Analysis document for further detail on backstop structures, OEM landscape, and underwriting comparisons.

19, Illustrative Cash Flows

What it is

Two directional cash flow shapes, DC and energy plant, over the project life. Not a financial model, just the shape that reveals the alignment problem.

Data center

Year 0-1: dev capital $50-80M. Year 1-3: construction $3-5B. Year 3: COD, lease begins, revenue ~$300-500M/year. Year 4+: stabilized, 3% annual escalators, 15-year lease tail.

Energy plant

Year 0-2: dev capital $125M plus turbine deposits $500M-$1.5B. Year 2-6: phased construction $2-2.5B drawn over 4-5 years. Year 4: Phase 1 first power 250 MW, partial revenue $80-100M/year. Year 6: full COD, full revenue $300-400M/year. Year 8+: stabilized, 15-20 year PPA.

The shape difference matters

The DC trough is deep but short, 2-3 years of negative, sharp inflection at COD.

The energy plant trough is deeper and longer, 4-6 years of negative, partial revenue starts mid-trough, full revenue much later.

The DC reaches stabilization in 3-4 years (developer hold-to-flip; long-term hold cash payback at 9-11% YoC is 9-11 years). The plant reaches stabilization in 6-8 years.

Equity returns compress on the energy side (8-12% unlevered) vs the DC side (8-10% stabilized but 25-40% during dev).

Why it matters

Different cash flow shapes force different financing structures. DC financing uses construction-to-perm rollover at COD. Energy financing uses staged construction debt with mini-perm conversion at full COD. The two cannot share a single capital stack without complicated tranching. The fundamental mismatch drives the need for either integrated platforms (one party bears both shapes) or carefully structured cross-stakeholder coordination where each party's capital is matched to the risk profile it can most efficiently bear. Deep Dive 30 covers the coordination frameworks.

Risk

Continuous on capital deployment timing.

Underwriting impact

Lenders look at peak negative cash and time to stabilization separately for each side. The energy plant's longer trough and later payback put more pressure on off-taker credit and PPA tenor than the DC's lease does.

20, Case Studies

Three deals from the last 18 months

Case 1: Google's $4.75B acquisition of Intersect Power's digital power assets (Dec 2025)